ROI (return on investment), typically expressed as a percentage, measures the profit or gain made on an investment compared to the original cost of that investment.

The three main ways investors factor their ROI on a rental property real estate investment are through monthly rent income minus expenses (i.e., cash flow), the potential appreciation in property value over the long term, and the tax benefits that rental property owners receive.

We’ll show you how to calculate the ROI of a rental property step by step, along with several different metrics investors use to calculate it.

How to calculate ROI on rental property

You can calculate ROI on a residential rental property using the following formula:

- ROI = (Gain on investment – Cost of investment) / Cost of investment

You can invest in real estate by paying cash or by financing the property. Let’s look at the ROI for a cash purchase compared to a financed purchase, using $100,000 in capital as an example. We’ll assume the property is sold after five years for $135,000.

ROI on a cash purchase

- Purchase price = $100,000

- Sale price = $135,000

- Gain on sale = $35,000

- Mortgage expense = $0

- Annual before-tax cash flow = $6,000 from rental income

Note: we’re not including property tax estimates here as they can vary widely from state to state.

Gain on investment = $6,000 before-tax cash flow x 5 years = $30,000 + $35,000 gain on sale = $65,000 + $100,000 return of initial investment

Annualized ROI using Compound Annual Growth Rate (CAGR)

CAGR = (Ending Value / Beginning Value)^(1/n) – 1

= ($165,000 / $100,000)^(1/5) – 1

= (1.65)^(1/5) – 1

= 1.1053 – 1

= 0.1053 or 10.53% per year

Total ROI

Total ROI = (Total Return / Initial Investment) x 100

= ($165,000 – $100,000) / $100,000 x 100

= ($65,000 / $100,000) x 100

= 0.65 x 100 = 65% over 5 years

The Compound Annual Growth Rate (CAGR) is used to calculate the annualized ROI. CAGR represents the rate at which the investment would grow each year if it grew at a steady rate, accounting for the compounding effect over time. This method provides a more accurate representation of annual returns for investments held over multiple years.

The difference between the annualized return (10.53%) and the total ROI (65%) is due to the time factor and compounding effect. The total ROI simply shows the overall return over the entire 5-year period, while the annualized return (CAGR) breaks this down into an equivalent yearly rate, assuming compound growth. This allows for easier comparison with other investments that might have different time horizons.

This CAGR calculator can help you figure out your own annualized return.

ROI on a financed purchase

- Purchase price = $100,000

- Down payment = $25,000

- Sale price = $135,000

- Gain on sale = $35,000

- Mortgage expense = $3,804 (principal and interest)

- Before-tax cash flow = $6,000 – $3,804 = $2,196

Gain on investment = $2,196 before-tax cash flow x 5 years = $10,980 + $35,000 gain on sale = $45,980

- ROI = ($45,980 – $25,000) / $25,000 = 12.96% annualized ROI with a total ROI of 83.92%

By financing the purchase of an investment property, an investor in this example generates 2.43% more in return on investment each year compared to paying all cash for the property.

ROI on multiple financed purchases

Continuing with our example of an investor with $100,000 in capital to invest, let’s assume that (with debt financing) four (4) rental properties could be purchased with a 25% down payment ($25,000) for each home instead of paying all cash for just one house.

Assuming the five-year return on each property is the same, the annualized and total ROIs would still be 12.96% and 83.92%, respectively. However, the actual total gain on investment from all 4 properties would be $183,920:

- $45,980 gain on investment per property x 4 properties = $183,920 total gain on investment

It’s also worth considering that by acquiring four (4) different properties, an investor could conceivably also diversify their portfolio geographically by purchasing rental houses in various parts of the country.

ROI on a one-year holding period

The above examples calculated the ROI over a multi-year holding period of a property being sold. You can also use a modified version of the ROI formula to calculate the return on investment for one year while you still own the property:

- ROI = Before-tax cash flow / Total investment

For the all-cash purchase, the one-year ROI is:

- $6,000 Before-tax cash flow / $100,000 Total investment = 6.0%

For the financed purchase, the one-year ROI is:

- $2,196 Before-tax cash flow / $25,000 Total investment = 8.8%

Other ways to calculate rental property returns

In addition to the ROI formula, there are countless other ways a real estate investor might calculate rental property returns. We’ll explore four additional approaches that are favored amongst savvy investors.

Net operating income

Net operating income (NOI) is the cash flow generated by a rental property after operating expenses are subtracted but before factoring in the mortgage expense. In our earlier example, when our investor purchased the property for cash, the before-tax cash flow of $6,000 was the NOI because there was no mortgage payment.

Cap rate

Cap rate (capitalization rate) is a calculation for comparing the current or expected returns from similar properties in the same market. The cap rate formula does not factor in the mortgage payment because investors purchase and finance rental property differently:

- Cap rate = NOI / Property value

- $6,000 NOI / $100,000 Property value = 6%

Real estate investors can also use the cap rate formula to calculate what a property’s value should be based on the market cap rate and projected NOI, and/or what the NOI should be based on the market cap rate and property value.

To calculate what the property value should be, rearrange the cap rate formula like this:

- Property value = NOI / Cap rate

- $6,000 NOI / 6% Cap rate = $100,000 Property value

To calculate what the NOI should be, rearrange the cap rate formula like this:

- NOI = Property value x Cap rate

- $100,000 Property value x 6% Cap rate = $6,000 NOI

Cash-on-cash return

Cash-on-cash return compares the annual before-tax cash flow to the total cash invested and uses the same calculations that the ROI formula for a one-year holding period does:

- Cash-on-cash return = Before-tax cash flow / Total cash invested

- $2,196 Before-tax cash flow / $25,000 Total cash invested = 8.8%

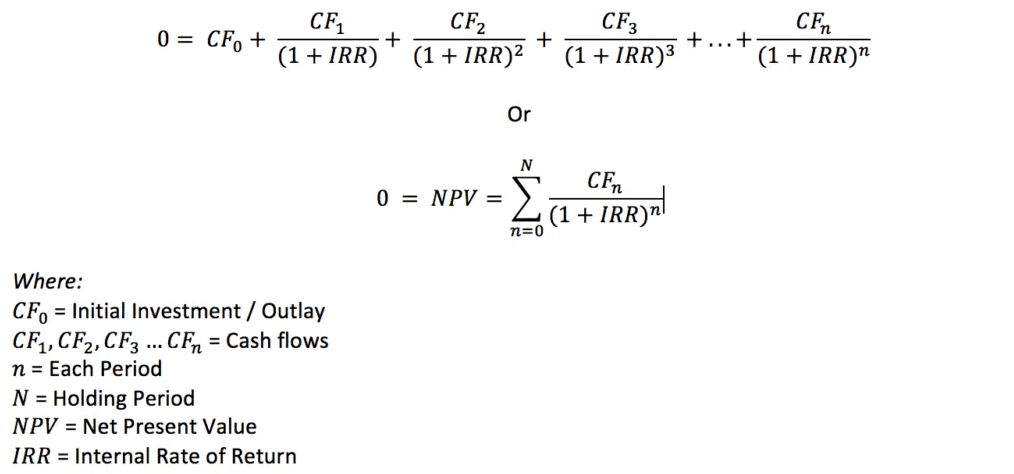

Internal rate of return

Internal rate of return (IRR) measures the value of the income and appreciation a property generates during the holding period, taking into account the time value of money. The IRR formula looks like this:

(Source: Corporate Finance Institute)

Using the internal rate of return formula, some mathematicians (and Excel) can calculate the IRR for the property as if it was purchased for cash (unlevered IRR) and with financing (levered IRR):

- Cash purchase: $100,000 purchase price, $135,000 sale price, $6,000 before-tax annual cash flow = 11.56% IRR

- Financed purchase: $25,000 down payment, $135,000 sale price, $2,196 before-tax annual cash flow = 14.75% IRR

While the IRR calculation is a good formula to calculate the potential return from a rental property, it’s also one of the most complicated.

To calculate IRR, you can use an online IRR Calculator or this simple spreadsheet. You can also use that spreadsheet to view projected key return on investment (ROI) metrics, including cash flow, cash-on-cash return, net operating income, and cap rate.

The easiest way to measure your ROI

Most rental property owners fail to track essential financial metrics properly or use a spreadsheet to manually calculate it — until they discover there’s a better way.

Introducing Stessa: software that helps rental property investors accomplish more in less time. With Stessa’s real-time dashboards and advanced reports, you can own and manage your rental properties like the pros.

Built for landlords, Stessa can generate interactive and clickable key reports so you can see the underlying transactions included in each calculation quickly and easily.

Stessa can also import, categorize, and index all your expenses seamlessly and securely. Connect to banks, lenders, credit cards, and property managers — all your data is in one place.

The Stessa platform also offers a wide range of essential tools landlords need to run their day-to-day operations, including:

- Smart receipt scanning: Add expense receipts to your transactions ledger quickly and accurately via mobile scans and email forwarding, reducing the risk of losing or misplacing vital receipts.

- Rental applications: Manage tenant applications efficiently and effectively by streamlining the process of publishing vacancies and collecting and reviewing applications.

- Tenant screening: Use a proprietary approach with RentPrep for comprehensive tenant checks, including a full credit report, background check, and more. Landlords can also add screening for income verification or of judgment and liens, increasing the odds of selecting reliable tenants.

- Online rent collection: Automate your rent collection process, including payment reminders and late fees, reducing the likelihood of missed or late payments.

- Landlord banking: Open FDIC-insured bank accounts and enjoy a more efficient way to manage your property-related finances. You can earn more than 10x the national average interest rate on every dollar deposited.*

- Mobile app (iOS and Android): Utilize Stessa’s mobile app to help manage your properties on the go. You can categorize transactions, check key metrics, scan receipts, and view your portfolio from almost anywhere, anytime.

- eSigning: Simplify lease signing and other document execution with integrated eSignature capabilities from DocuSign. This feature makes it easier for landlords and tenants to sign important documents, reducing the need for in-person meetings.

- Tax center: Tax time is a cinch thanks to the Stessa Tax Package feature. It helps aggregate your transactions and sends you personalized tax reports via email with digital copies of all of your receipts packaged into a single ZIP file.

Learn why over 250,000 landlords use Stessa. Get started for free.

*Stessa is a financial technology company and is not a bank. Banking services provided by Thread Bank, Member FDIC. The Stessa Cash Management Visa® Debit are issued by Thread Bank pursuant to a license from Visa U.S.A. Inc. and may be used everywhere Visa cards are accepted.

Your deposits qualify for up to $3,000,000 in FDIC insurance coverage when placed at program banks in the Thread Bank deposit sweep program. Your deposits at each program bank become eligible for FDIC insurance up to $250,000, inclusive of any other deposits you may already hold at the bank in the same ownership capacity. You can access the terms and conditions of the sweep program at https://thread.bank/sweep-disclosure/ and a list of program banks at https://thread.bank/program-banks/. Please contact customerservice@thread.bank with questions regarding the sweep program.

No minimum balance or opening deposit required. Fees could reduce earnings on the account. Account holders can earn 1.10% cash back on debit card purchases. Cash back earned each month will be credited to your account by the next month’s statement cycle. ATM transactions, the purchase of money orders or cash equivalents, loan payments and account funding made with your debit card are not eligible for cash back rewards. Terms and eligibility requirements apply.

Essentials is a free plan and Manage and Pro are premium subscription plans. The terms and conditions for Stessa Plans are subject to change, including pricing. Annual Percentage Yield (APY) of 2.45% on deposit accounts for new Essentials and Manage users signing up, accurate as of December 17th, 2024; and 4.23% APY for Pro users is accurate as of December 17th, 2024. APY for the account may change at any time, before or after the account is opened.

Stessa does not provide tax, legal or accounting advice. This material has been prepared for informational purposes only, and is not intended to provide, and should not be relied on for, tax, legal or accounting advice. You should consult your own tax, legal, or accounting advisors.